The Physical AI Reference Stack

Why three commercial humanoid contracts in 2026 decide factory compute through 2030.

By Armando Pereira | Founder, PVentures Consulting | Senior Member IEEE | Co-founder, OpenFog Consortium (IEEE 1934) | President, Autonomous Vehicle Computing Consortium | Former VP/GM Optical BU, Centillium Communications (CMOS PON SoC, NTT-qualified)

👋 Welcome back to The Vector™

The Vector™ is the bi-weekly directional deep dive for execs, founders, and investors operating in deep tech. Each issue tracks a single development, technology shift, regulatory move, or competitive realignment to its directional endpoint: where it is heading, how consequential it is, and what the next ninety days will force you to decide.

🎯 Why Now

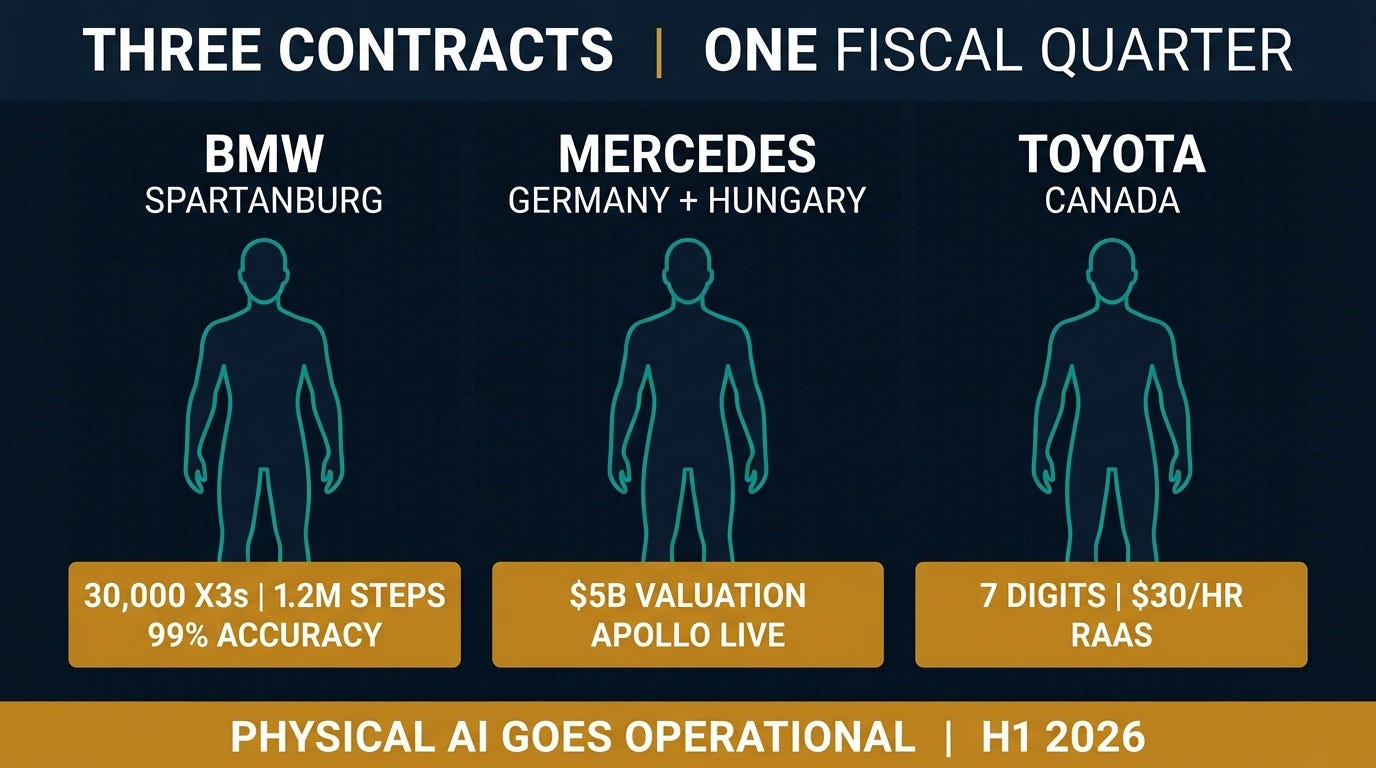

Three commercial humanoid contracts were awarded in the first half of 2026 at three Tier 1 automotive OEMs.

BMW closed an 11-month pilot at Plant Spartanburg with Figure 02, which supported the production of more than 30,000 BMW X3 vehicles, handled 90,000 components, logged 1.2 million steps, and recorded 1,250 operating hours, achieving 99% placement accuracy per shift.

BMW announced on 27 February that the AEON humanoid, sourced from Apptronik, will move into Plant Leipzig starting in summer 2026 for high-voltage battery assembly and component manufacturing.Apptronik closed a Series A-X round of $520 million in February at a $5 billion valuation, with Mercedes-Benz, Google, AT&T Ventures, John Deere, and Qatar Investment Authority participating.

Agility Robotics signed a Robots-as-a-Service contract with Toyota Motor Manufacturing Canada in February, with seven Digit units entering the RAV4 line at Woodstock, Ontario, in April at a published rate near $30 per hour, targeting a sub-2-year payback against fully loaded human cost. The hourly figure is the most consequential number in the set; it converts the humanoid debate from a research question into a line item on a manufacturing OPEX budget.

That is not a pilot wave. That is three Tier 1 OEMs signing commercial contracts for humanoid platforms in the same fiscal quarter. The consensus reading is that 2026 is still hype and that real scale arrives between 2027 and 2030. The numbers underneath BMW’s 30,000-car proof, Apptronik’s near-billion-dollar Series A, and Agility’s hourly billing model say something else.

The question that matters now is not whether humanoids work on a line. It is unclear which compute substrate, which foundation model, and which orchestration layer will become the de facto reference architecture for factory IT through 2030.

The boards that answer that question this quarter will write the playbook the rest of the sector copies.

🧭 The Thesis This Week

Consensus: 2026 is a pilot year; humanoid robots remain experimental, and economic viability is unproven.

The Vector™ position: three commercial contracts inside the first half of 2026, anchored by 30,000 vehicles of production data at BMW and a published per-hour rate at Toyota, have already moved the question past viability; the real exposure has shifted to the compute substrate (NVIDIA IGX Thor versus Qualcomm Dragonwing IQ10) and the foundation-model layer (NVIDIA Isaac GR00T versus proprietary VLA models) that lock OPEX for the next decade.

Endpoint: by Q4 2027, one or two reference stacks reach commercial production at Tier 1 OEMs, and switching cost on the chosen stack exceeds three years of factory IT OPEX.

Grade: within 90 days, watch whether another Tier 1 OEM commits to a single named compute substrate for a factory build (the consolidation signal) or whether the BMW, Mercedes, and Toyota stacks diverge publicly (the fragmented signal).

📌 What Execs Should Do This Quarter

Inventory the factory IT compute roadmap against the physical-AI vendor map.

If your CIO and CTO cannot name the compute substrate (IGX Thor, Dragonwing IQ10, or proprietary) on the humanoid platform you are piloting or considering, the procurement decision is being made one layer down by your vendor, not by you. Treat this as the silicon question, not the robot question.Push the supplier base for ISO 25785-1 readiness statements.

The standard for dynamically stable robots remains a working draft with publication expected in late 2026 or 2027. ISO 10218-1:2025 covers collaborative applications but not the walking-robot fall-zone case. If a vendor cannot describe how its safety case will migrate when ISO 25785-1 lands, the deployment timeline is shorter than the slide deck.Stress-test the RaaS pricing claim with finance.

Agility’s published rate of approximately $30 per hour, with sub-2-year payback against fully loaded human cost, is the public number to model. If your finance team cannot reconcile it against a real cell on your floor, the gap is the missing OPEX (downtime, charging, integration labor) that vendors strip out of pilot economics.Add a physical-AI exposure line to the operational risk register.

The exposure is not the robot; it is the multi-year compute and foundation-model commitment underneath it. Three years of OPEX on the wrong stack is the failure mode, not a robot dropping a fender.

The full mechanism, vendor map, scenario probabilities, and board-ready exposure matrix are in the paid extension below.

🎯 Upgrade to Read the Full Analysis

If you are a CIO, CTO, board director, head of operations, or fractional executive making capital allocation decisions inside manufacturing through 2027, the paid extension translates this directional argument into the named-vendor matrix, the counter-argument from Morgan Stanley’s wealth research desk, the on-the-record quote from BMW’s Board Member for Production, and a 4-layer exposure framework you can run against your factory IT roadmap inside an hour.

The paid extension also tightens the standards-body framing for risk counsel and the named-vendor concentration view for board directors deliberating capital allocation.

The Vector™ is built to be a permanent reference asset, not just a weekly read.