The Network Gets a Brain!

How MWC 2026 confirmed AI-native infrastructure as the control layer for factories, vehicles, and physical AI.

👋 Welcome back to TechThoughts™

TechThoughts™ is a weekly deep dive into trending developments across one of four focus markets: Industrial IoT, Telecommunications, Edge Computing, and Autonomous Vehicles. This curated newsletter unpacks the details and explains their significance for business leaders and investors, fueling your strategic thinking.

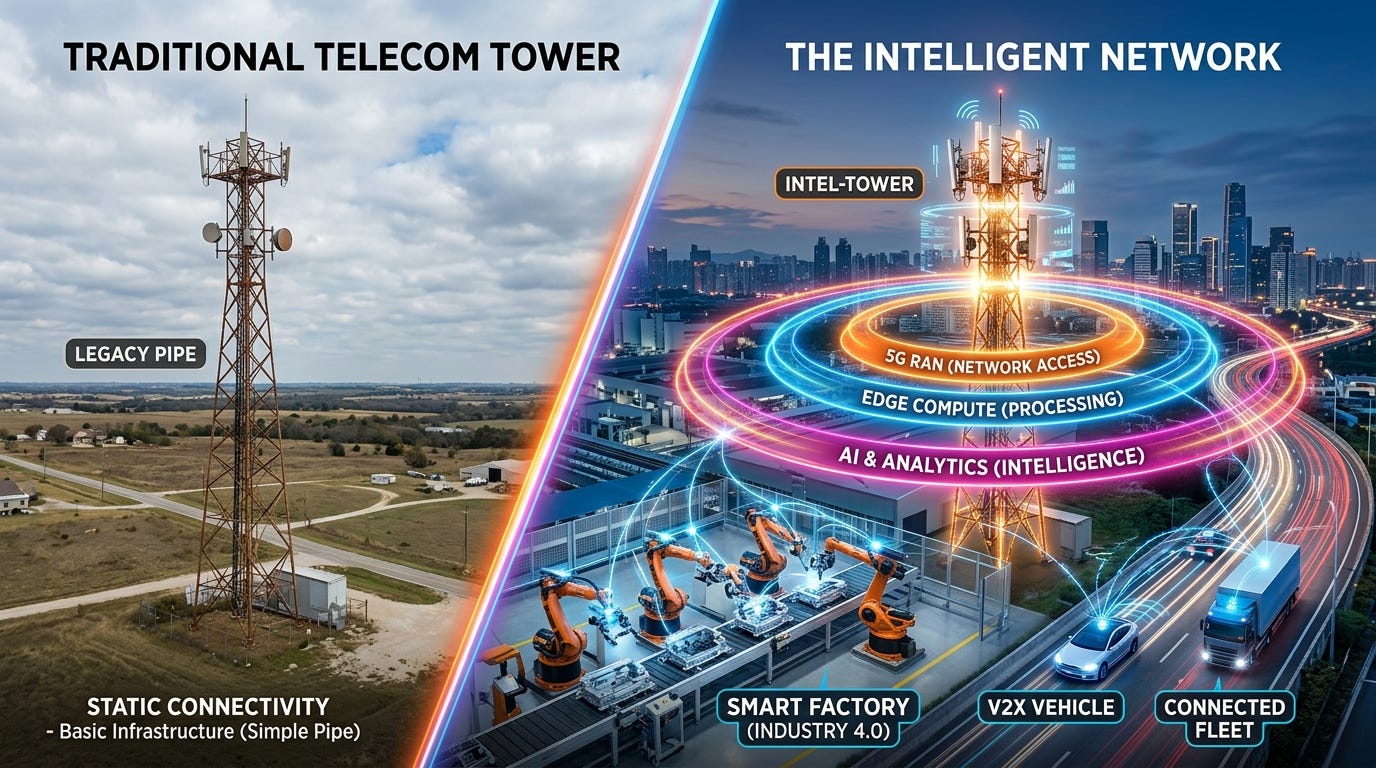

For a decade, Mobile World Congress served up the same promise: 5G will transform everything. What changed in Barcelona this March was the proof. MWC 2026 did not showcase faster pipes or incremental radio upgrades. It showcased a convergence of AI, 5G RAN, and edge compute running as one unified stack, explicitly aimed at factories, autonomous vehicles, and industrial robotics. The telecom operators standing in the FIRA halls were no longer selling bandwidth. They were selling a distributed control plane for the physical world.

The tension is structural. Industrial and automotive systems demand sub-millisecond determinism, on-site data sovereignty, and always-on reliability. Cloud-centric AI cannot deliver any of those properties. The industry needed a new architecture, and MWC 2026 arrived with three convergent proof points, from Qualcomm and Siemens on the factory floor, from Wind River and Nvidia in the RAN, and from Intel at the edge compute layer, that together signal a genuine transition from concept to early production. Executives who treat this as a future roadmap item will be executing catch-up programs by 2027.

✅ The 3 Verified Signals

Signal 1: The supply chain has aligned silicon, software, and RAN for AI-native networks.

→ NVIDIA and Quanta Cloud Technology (QCT) announced off-the-shelf AI-RAN products embedding NVIDIA GPU platforms and Nokia software directly into the RAN, enabling enterprise AI workloads to run at the network edge. 77% of NVIDIA survey respondents expect faster deployment of AI-native wireless architectures versus prior generations. SIMCom’s 12 TOPS AI modules (SIM9650W) are already deployed across automotive, robotics, and industrial domains.

→ Intel’s Network & Edge Group demonstrated live-network AI inference on a single open platform for 5G across manufacturing, retail, and critical infrastructure.

Signal 2: Concrete industrial and automotive edge-AI deployments have moved from lab demos to early production.

→ Qualcomm and Siemens demonstrated an on-premises industrial AI and private 5G factory model at MWC 2026 featuring coordinated AGVs and robotic arms over Siemens industrial 5G, with local AI inference running on Qualcomm Cloud AI 100 accelerators for real-time diagnostics and quality inspection.

→ Wind River ran a live C-V2X software-defined vehicle demo and a physical-AI robotic arm demo, highlighting ultra-low-latency edge control.

→ Capgemini showcased a humanoid robot controlled via real-time edge processing over private 5G.

→ Haivision deployed an airborne private 5G network for live video contribution and public-safety workflows—operational, not lab.

Signal 3: Networks are being repositioned as distributed AI-edge platforms, not connectivity pipes.

→ GSMA’s MWC 2026 themes, ’ConnectAI’ and ‘Intelligent Infrastructure’, explicitly frame networks as receiving ‘brains as well as bandwidth,’ with distributed AI at the edge, self-optimizing radios, and AI-automated slicing and operations positioning telecom as a strategic value platform for industrial capabilities.

→ Moso Networks cited forecasts of up to $8B in annual enterprise private 5G spend by 2026 with 30–45% YoY growth as deployments shift from pilot to mission-critical.

→ Intel stated that more than one-third of enterprise workloads are expected to migrate from centralized data centers to edge environments by 2028.

🧠 My Thesis This Week

The single most important takeaway from MWC 2026 is this: the AI-native, edge-driven telecom infrastructure is becoming the de facto control layer for industrial IoT and autonomous systems. This is not a future roadmap item; it is an early-production reality confirmed by three independent proof points from Qualcomm/Siemens, Wind River/NVIDIA, and Intel, each targeting different layers of the same stack.

The convergence of AI, 5G RAN, and MEC is not additive; it is architecturally fused. Connectivity without embedded intelligence is being commoditized. The organizations that treat this stack as infrastructure, like cloud compute or power, and build operational models around it, will compress their IoT and automation deployment cycles by years.

The strategic risk is fragmentation. The ecosystem now spans NVIDIA, Intel, Qualcomm, QCT, Moso, SIMCom, Wind River, and Capgemini, each owning a layer. Enterprises that assemble point solutions will own the integration debt. The playbook is to select open, cloud-native architectures aligned to 3GPP, O-RAN, and TM Forum ODA, and to insist on integrators with demonstrated multivendor deployments. The window to establish architecture governance is open now, before the stack consolidates around two or three platform vendors.

📌 What Execs Should Do Next Quarter

Conduct an AI-native infrastructure audit against this stack.

→ Map your current private 5G, MEC, and edge AI assets against the four-layer model (RAN → MEC → AI runtime → application control). Identify where your architecture has gaps versus the production-grade deployments demonstrated at MWC 2026 by Qualcomm/Siemens and Capgemini. This audit should produce a single-page architecture delta document for your board.Qualify two to three integrators with multivendor AI-RAN credentials.

→ The supply chain is mature enough that you should be issuing RFIs to integrators who can demonstrate O-RAN-compliant deployments combining NVIDIA/QCT AI-RAN hardware, Wind River or equivalent cloud-native stacks, and private 5G from vendors such as Moso or Siemens. Do not accept RFP responses that propose a single-vendor lock-in without O-RAN alignment.Model payback for a private 5G + edge AI pilot anchored to a specific OT failure mode.

→ Select one high-frequency failure mode in your factory or fleet (unplanned downtime, quality inspection misses, or logistics AGV collisions). Build a baseline cost model and define the latency, reliability, and inference accuracy requirements for a private 5G + edge AI deployment. This becomes your business case for board approval and your benchmark for vendor evaluation in Q3.

🔒 Inside the Board Pack

Blueprint: Four-layer AI-native control plane architecture with ASCII diagram and per-layer vendor assignments.

Decision Tree: Six-step decision framework for choosing between operator MEC, private 5G on-prem MEC, and hybrid edge topologies for industrial use cases.

Vendor Map: Full who-profits table across seven stack layers (RAN, edge silicon, AI runtime, OSS/automation, industrial integration, C-V2X, and platform) with watch signals for the next 180 days.

Constraint Table: Six confirmed failure modes (latency, thermal, OT integration, AI model drift, fragmentation, ROI uncertainty) with specific mitigations sourced from the Fact Base.

Unit Economics Template: CAPEX and OPEX variable tables, core ROI formulas, and sensitivity levers for private 5G + edge AI deployments.

6-Step Implementation Roadmap: From architecture audit to multi-site production, including governance RACI.

Watch List (30–180 Days): Five named signals, three scenarios (Best/Base/Risk) with probability estimates.

🎯 Upgrade to Unlock the Board Pack

Upgrade to unlock the Board Pack tables, templates, and the step-by-step blueprint that turns this thesis into a board-ready deployment plan.

Subscribers get a new issue every Thursday.

12 months compound into a genuine technology edge.