The Humanoid Deployment Gap

Factory references, not dexterity demos, will sort the robotics winners

By Armando Pereira | Founder, PVentures Consulting | Senior Member IEEE | Co-founder, OpenFog Consortium (IEEE 1934) | President, Autonomous Vehicle Computing Consortium | Former VP/GM Optical BU, Centillium Communications (CMOS PON SoC, NTT-qualified)

👋 Welcome back to The Vector™

The Vector™ is the bi-weekly directional deep dive for execs, founders, and investors operating in deep tech. Each issue tracks a single development, technology shift, regulatory move, or competitive realignment to its directional endpoint: where it is heading, how consequential it is, and what the next ninety days will force you to decide.

🎯 Why Now?

Figure hit roughly one robot per hour on its BotQ line in May, up from one per day 120 days earlier, a 24x throughput gain, on a facility rated for 12,000 units a year with a stated path to 100,000, months after closing a $1 billion Series C at a $39.5 billion valuation.

On 24 June, Morgan Stanley doubled its China humanoid shipment forecast; Unitree, cleared for a roughly $610 million Shanghai IPO at about $6.2 billion, posted its first profitable year in 2025 and is targeting 20,000 units in 2026.

Tesla, meanwhile, is targeting Optimus V3 production at Fremont this summer, on the line freed up when Model S and Model X production ended in May.

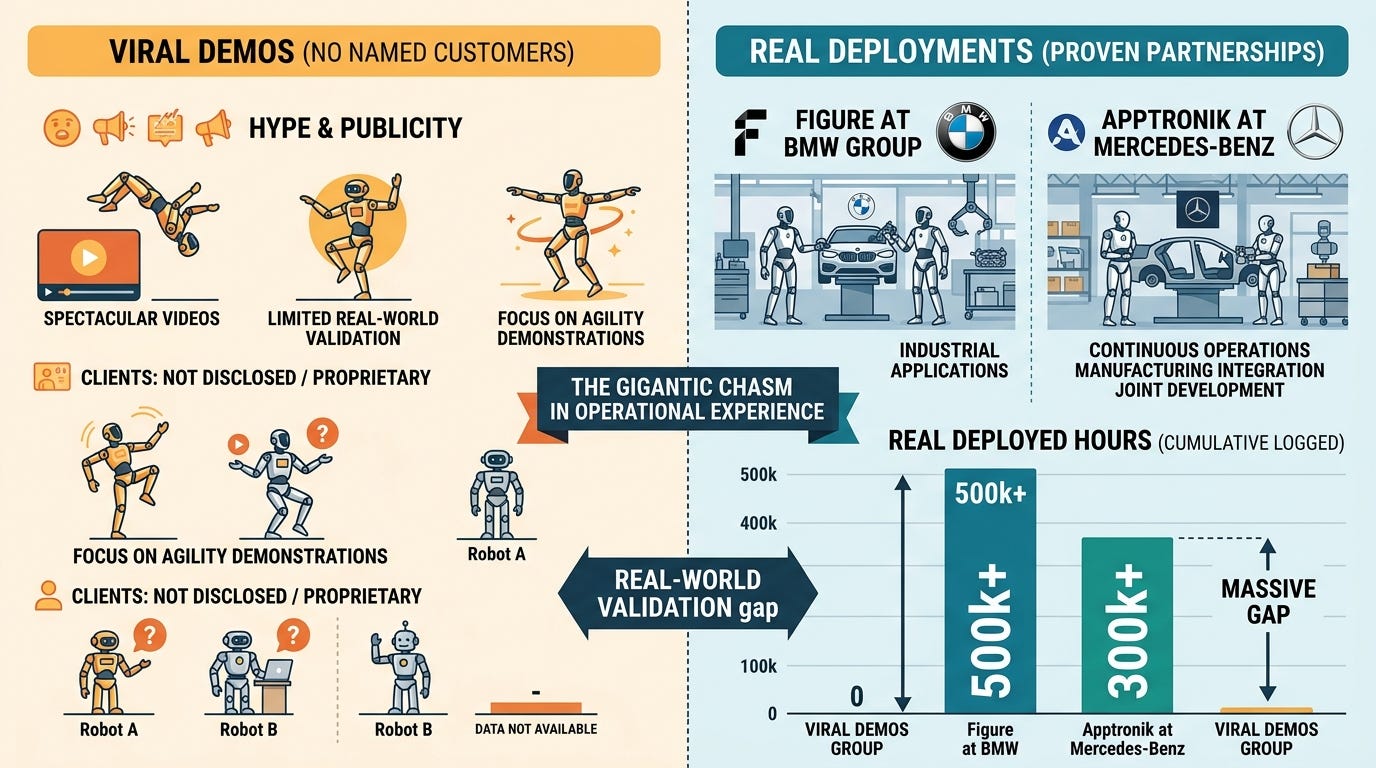

Read together, these look like a capability race, the contest to build the smartest, most dexterous robot. They are not. The companies pulling away are the ones with paid operating hours inside a named customer’s plant, and the ones shipping cheap units at volume. Viral dexterity demos are filling social feeds; they are not filling order books. A robot that can fold laundry on a research bench and a robot that has run 1,250 shifts in a body shop are separated by the exact gap that procurement committees care about. The asset is not the robot. It is the reference deployment.

🧭 The Thesis This Week

Consensus: humanoid robotics is an AI-capability race; whoever builds the smartest, most dexterous machine wins the market.

The Vector position: it is a deployment race. The moat is paid operating hours inside a named customer’s production system, plus throughput per line, not demo dexterity.

Endpoint: by the end of 2027, the market sorts into two proven tracks: a Western integrated-reference path (Figure at BMW, Apptronik at Mercedes-Benz) and a Chinese volume-and-price path (Unitree, AgiBot); vendors with no production reference and no volume lose enterprise procurement regardless of demo quality.

Grade: watch whether a second automaker publishes multi-month, multi-thousand-vehicle deployment data in the BMW-Spartanburg mold within 90 days. If only demos and unit-shipment forecasts appear, the gap is widening, not closing.

📌 What Execs Should Do This Quarter

Separate the demo from the deployment.

A viral clip of a robot folding laundry is a research result, not a procurement signal. Track which vendors can name a customer, a task, a shift pattern, and a duration. Everything else is marketing.Ask for reference data, not spec sheets.

BMW disclosed 30,000-plus vehicles, 90,000-plus components, and roughly 1,250 operating hours from a single Figure deployment. That is the unit of proof. Demand the equivalent before you pilot.Fix your data platform before your robot.

BMW’s precondition was a unified production data model and a Smart Robotics ecosystem with standardized interfaces. Physical AI rests atop an edge and data substrate; without it, a humanoid is an expensive island.Price both paths deliberately.

An integrated-reference robot carries a premium and a support relationship. A Unitree-class unit at roughly 4,290 to 16,000 dollars carries neither, and neither a factory reference. Decide which problem you are buying for before you compare quotes. A premium reference unit and a low-cost volume unit are not competing products; they answer different questions, and confusing them is the fastest way to overpay or underdeliver.

The full mechanism, vendor map, scenario probabilities, and board-ready exposure matrix are in the paid extension below.

🎯 Upgrade Call to Action

This issue is written for the executive deciding whether to fund a humanoid pilot in 2026, the operator weighing an integrated-reference vendor against a low-cost unit, and the investor separating deployment moats from demo hype. The paid extension carries the deployment flywheel, the named vendor and investor landscape, the counter-argument with three bear-case signals, the Deployment Proof Matrix, three scenarios to 2027, and a public-company snapshot.