TechPulse™ Week 16: Edge Takes Command. Autonomous Scale Forces a Hardware Reckoning

From military robotics to robotaxis, AI's next infrastructure shift is physical, local, and already funded.

👋 Welcome back to TechPulse™

TechPulse™ is your weekly operating brief for execs, founders, and investors: what changed, why it matters, and what to do next in Industrial IoT, Telecommunications, Edge Computing, and Autonomous Vehicles, all in one place.

IN THIS ISSUE: The defense contract that signals autonomous robotics have crossed from R&D to deployment budgets, the spectrum milestone that sets the clock for 6G procurement, and the Board Memo your peers are already using to reposition edge infrastructure spend before Q3.

🩺 This Week’s Pulse

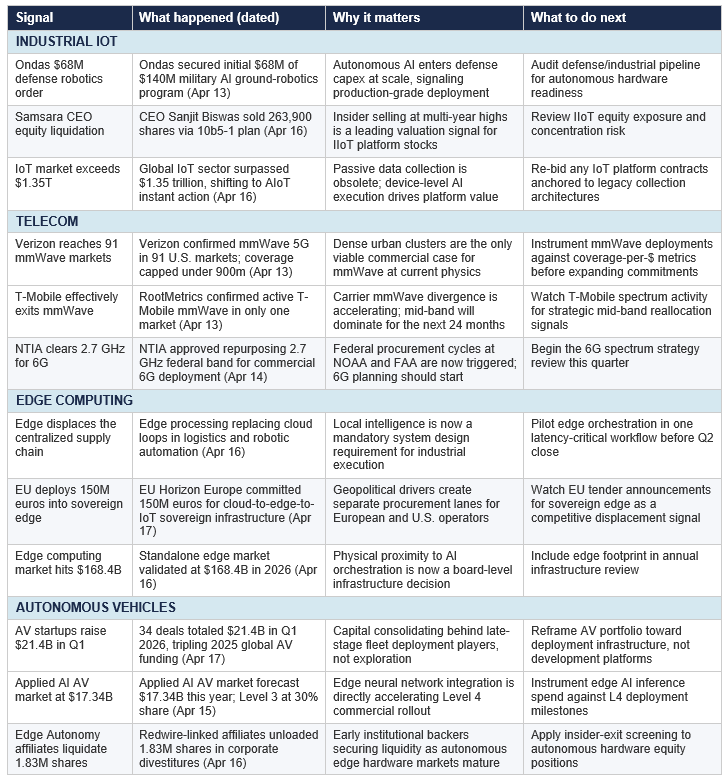

The week of April 13-17, 2026, delivered the clearest evidence yet that autonomous systems have left the pilot phase. A $68M military robotics order, a $21.4B surge in AV private funding, and a 150M euro European sovereign edge commitment arrived in the same five-day window, while two insider equity moves at IIoT platform leaders sent a quieter but equally important signal about sector valuation.

The NTIA cleared a milestone for 6G spectrum repurposing at 2.7 GHz, setting a federal procurement clock that few commercial planners have factored into their roadmaps. The architecture of the week was clear: capital is flowing toward the physical layer -- edge compute, spectrum, and autonomous hardware -- and away from the platform software abstractions that absorbed investment for the prior decade.

The company that actually benefits most from the AV capital rotation is not the one making the largest headlines. That name is in today’s Board Pack.

MY THESIS THIS WEEK

As autonomous systems cross from pilot to fleet deployment in both defense and commercial markets, the infrastructure requirement shifts decisively from cloud-centric platforms to edge-native compute, deterministic networking, and physical hardware security -- and operators who have not restructured their procurement stack by Q3 2026 will face a two-to-three quarter lag in deployment readiness.

🔒 Upgrade breadcrumb: The 90-day Board Memo, KPI thresholds tied to edge infrastructure RFPs, and the risk register linked to this thesis.

📌 Last Week’s Quick Intelligence

🔥 3 Non-Obvious Takeaways

Takeaway 1: Defense is now the fastest edge compute procurement channel.

PATTERN: The defense sector is running ahead of commercial markets on autonomous edge deployment, creating a procurement template that commercial operators can reverse-engineer.

EVIDENCE: Ondas secured a $68M first phase of a $140M multi-year autonomous ground robotics program described as ‘mission-integrated’ AI. This is not an R&D grant; it is a production deployment contract.

WHY THIS MATTERS: Whoever controls the defense edge compute playbook controls the commercial reference architecture for the next wave of industrial autonomy.

🔒 Upgrade breadcrumb: The named prime contractor relationships, the threshold deployment timeline, and the 90-day procurement move for commercial operators are in Board Memo Section 1.

Takeaway 2: mmWave is a Verizon story, not an industry story.

PATTERN: The carrier divergence on mmWave has reached a point where the technology is effectively a single-operator deployment.

EVIDENCE: Verizon operates in 91 mmWave markets; T-Mobile’s active mmWave presence was confirmed by RootMetrics in just one market. The physics constraint - coverage capped under 900 meters - has not changed.

WHY THIS MATTERS: Infrastructure planners treating mmWave as a broadly available 5G substrate are building on a single-vendor dependency with structural coverage limits.

🔒 Upgrade breadcrumb: The threshold carrier concentration ratio that should trigger a re-RFP, and the 90-day network diversification move, are in Board Memo Section 2.

Takeaway 3: $21.4B in AV funding is a consolidation story, not a growth story.

PATTERN: Record AV capital in Q1 2026 masked a structural compression: fewer deals, much larger checks, directed at a handful of late-stage platforms.

EVIDENCE: 34 deals totaled $21.4B in Q1 2026, tripling global 2025 totals. A single Series D round accounted for a disproportionate share of that capital.

WHY THIS MATTERS: Investors still writing checks to early-stage AV development platforms are effectively competing for the remaining crumbs; the real deployment-layer opportunity has already been priced.

🔒 Upgrade breadcrumb: The named company capturing the largest single check, the secondary plays our Watchlist identifies, and the entry threshold for deployment-layer infrastructure investment are in Board Memo Section 3.

🧠 One Contrarian Take

CONSENSUS VIEW: The NTIA’s 2.7 GHz milestone is a 6G signal for the next decade.

OUR TAKE: The 2.7 GHz band approval accelerates commercial 6G trials into a 2027-2028 window, not 2030, because federal procurement at NOAA and FAA is now actively incorporating spectrum repurposing into ongoing procurement cycles, measured in quarters rather than years.

EVIDENCE: The NTIA press release explicitly stated that this approval enables the two primary federal users of the band to incorporate spectrum repurposing into their ongoing procurement. Federal procurement cycles are measured in quarters, not years.

🔒 Upgrade breadcrumb: The trigger condition, commercial trial window, and instrumentation checklist are in the Board Pack.

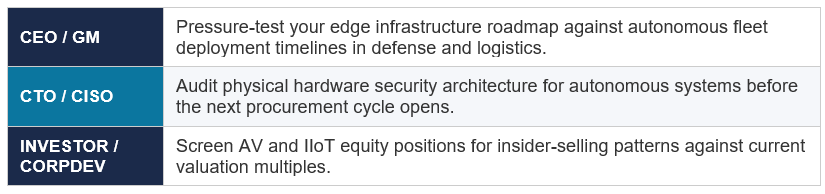

✅ If You Only Do 3 Things Next Week...

📣 Upgrade Call to Action

This week, paid subscribers see:

The named company, whose Series D round captures the majority of AV deployment-layer value in 2026, plus the two second-order plays our Watchlist identifies as underpriced.

The exact mmWave carrier concentration threshold that should trigger a network re-RFP before Q3, including the instrumentation cadence and owner.

Our Base/Upside/Downside probability split on the 6G commercial trial timeline, with the two leading indicators we are watching to confirm or kill that call.

If you are making infrastructure, spectrum, or autonomous systems decisions this quarter, the Board Pack is built to run inside your next executive meeting.