👋 Welcome to The Vector™

The Vector™ is the weekly directional deep dive for execs, founders, and investors operating in deep tech. Each issue tracks a single development, technology shift, regulatory move, or competitive realignment to its directional endpoint: where it is heading, how consequential it is, and what the next ninety days will force you to decide.

🎯 Why Now

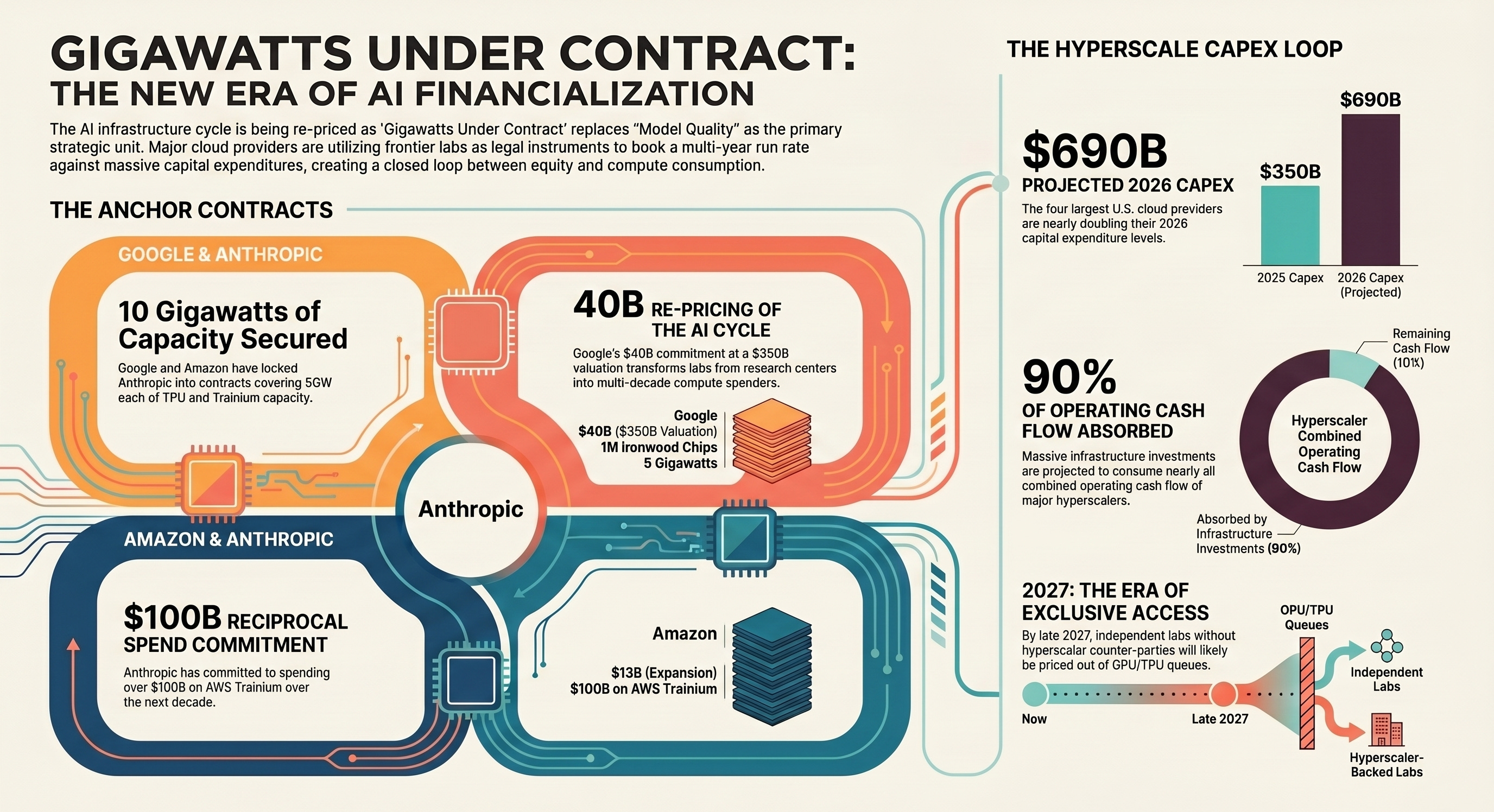

Last week, two contracts re-priced the AI infrastructure cycle. On April 24, Google committed up to $40B to Anthropic at a $350B valuation, plus 5 gigawatts of TPU capacity over five years and access to up to one million Ironwood chips. Four days earlier, Amazon expanded its Anthropic position to roughly $13B in equity against Anthropic’s reciprocal commitment to spend more than $100B on AWS Trainium over a decade, also covering 5 gigawatts. In one week, Anthropic was re-priced from a research lab into a multi-cloud, multi-decade compute spender with 10 gigawatts of capacity under contract.

These are not AI bets. They are the legal instruments by which the cloud books a multi-year run rate against the capex it has already announced, while taking equity in the entity that consumes that capacity. The four largest U.S. cloud providers have guided to roughly $690B in 2026 capex, nearly double 2025. Bank of America projects that figure accounts for close to 90% of their combined operating cash flow. The frontier lab has become the financing layer that converts hyperscaler balance sheets into committed compute revenue.

🧭 The Thesis This Week

Consensus: Google’s $40B is a strategic AI bet, a hedge against OpenAI on Microsoft, a play on Claude’s enterprise traction.

The Vector position: the foundation model layer is being financialized; the strategic unit is no longer parameters or model quality, it is gigawatts under contract, and the contracts have already been signed.

Endpoint: by the close of 2027, two or three frontier labs operate as multi-cloud, multi-silicon compute consumers under decade-long commitments; independents without a hyperscaler counterparty get priced out of the GPU and TPU queues that matter.

Grade: if Q3 2026 hyperscaler earnings show a third frontier lab signing at $25B+, the closed loop thesis is confirmed; if no second-tier lab signs at scale by Q4, this call is early.

📌 What Execs Should Do This Quarter

Audit AI exposure by silicon family, not by model family.

Claude on Bedrock, Claude on Vertex, and Claude direct converge to the same silicon roadmaps and the same cloud lock-in. Ask your AI lead for a written exposure map across TPU, Trainium, Blackwell, and Rubin.Change what you negotiate in your next AI contract.

Stop optimizing per-token pricing. Start fighting on capacity floors, silicon optionality, and data-portability rights. The terms that matter in 2026 are the ones that protect your switching options in 2028.If you own power, fiber, or interconnect, you are scarce input.

PJM projects a 6 GW shortfall by 2027. ERCOT’s 2030 data-center demand jumped from 29 to 77 GW in a single planning cycle. Reprice your counterparty list against AI capex.Track antitrust posture filings.

The January 2025 FTC staff report flagged consultation, control, and exclusivity rights. Google-Anthropic mirrors Microsoft-OpenAI and Amazon-Anthropic in form. A coordinated EU/FTC probe is the base case.

The full mechanism, vendor map, scenario probabilities, and board-ready exposure matrix are in the paid extension below.

🎯 Upgrade Call to Action

If you are making AI procurement, infrastructure, or capital-allocation decisions in the next 90 days, the paid extension is built to run inside your next executive meeting. Upgrade to a paid subscription of The Fog Signal™ for the full edition of TheVector™ every Thursday, and The Sextant™ board pack every other Wednesday.